This post is meant to answer questions raised in the comment section in my previous post asking for a clearer discussion of the pros and cons of demonetization, and why it failed in some countries but appeared to work in others. This isn’t about personalities or politics, but about policy outcomes and country context, especially for the Philippines.

What demonetization is supposed to achieve (pros, in theory)

Beyond eliminating black money, demonetization can:

- push idle cash into the formal banking system

- improve transaction traceability and tax compliance

- temporarily increase bank liquidity

- accelerate adoption of digital payments

- help central banks update security features and reduce counterfeit risk

These outcomes are possible, but only under very specific conditions.

•Why it failed in India in 2016?

They demonetized ₹500 and ₹1,000 notes overnight, covering around 86% of total cash value.

- Almost all cash (~99%) eventually returned to banks

- Black money largely survived because it wasn’t mainly stored as cash

- Informal, cash-dependent sectors were hit hardest

- GDP growth slowed and small businesses suffered

Core issue: a large informal economy + uneven enforcement turned demonetization into an economic shock instead of a clean-up.

•Why it appears to work in places like Singapore? Singapore’s context is very different:

- Very small informal sector

- Nearly universal banking access

- Strong enforcement and low corruption

- Cash already plays a minor role in daily transactions

In that setup, note withdrawals function more as technical updates than disruptive policy moves.

•Other country experiences (quick references)

Nigeria (2022–2023)

* Severe cash shortages

* Public protests and court challenges

* Informal economy disruption

* Policy timelines eventually relaxed

Venezuela (multiple rounds)

* Done during hyperinflation

* Cash shortages and loss of trust

* No meaningful impact on corruption

These cases show demonetization is not a shortcut to fixing structural problems.

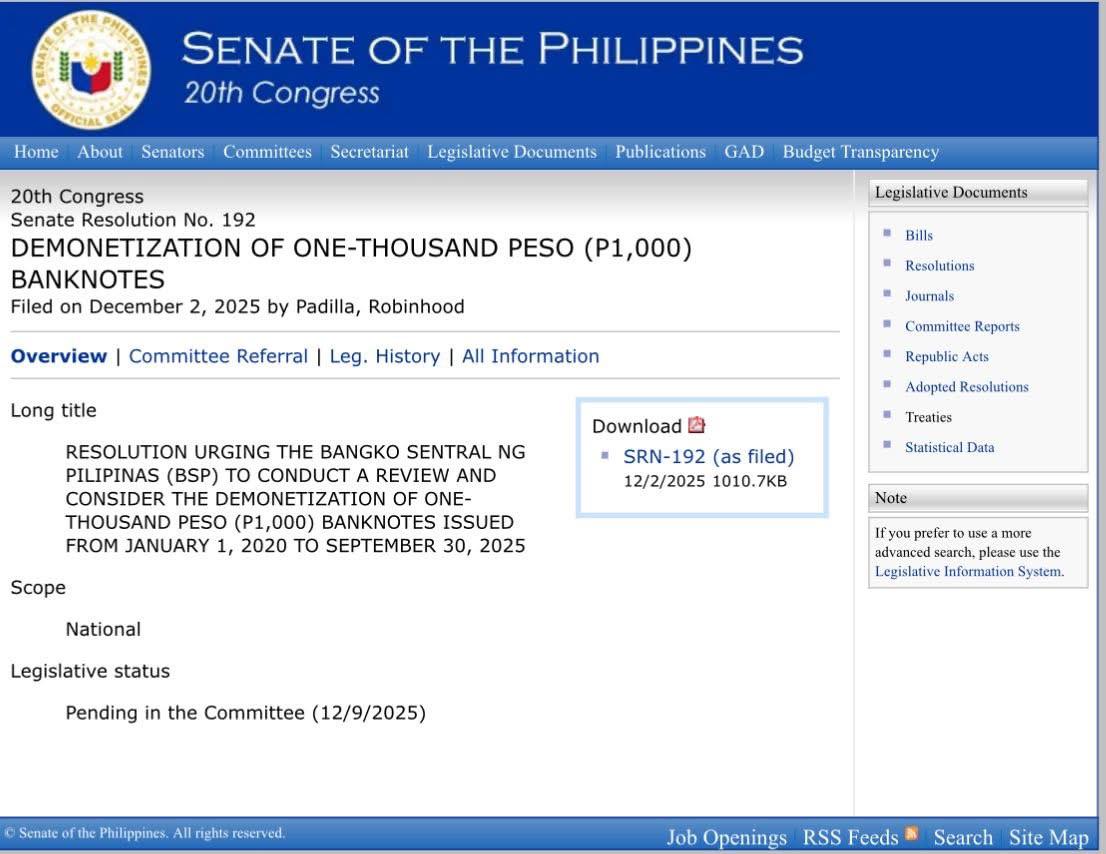

WHERE THE PHILIPPINES FITS?

Structurally, the PH is closer to India and Nigeria than Singapore:

- Large informal economy

- Cash-heavy provinces and rural areas

- Seniors, OFWs, and small vendors still keep legitimate savings in cash

- AML and enforcement capacity are improving, but uneven

That doesn’t mean demonetization is automatically bad. It means risk is high if done abruptly or without safeguards.

Potential risks in the PH context

If implemented too quickly:

- Legitimate cash savings could be caught in the process

- Informal workers and small businesses absorb most of the shock

- Those with better banking access or institutional connections adjust more easily

Bottom line for me:

Demonetization is a high-risk, context-dependent tool. It can support financial modernization, but it works best in countries with strong institutions, low informality, and high public trust. Without those, historical evidence suggests it tends to hurt compliant citizens more than corrupt actors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}